Cost Analysis in MTO: 9 Key Evaluations for Successful Cost Management

TL;DR: Make-to-order manufacturers face unique cost management challenges because every order is different, making it difficult to track expenses, set accurate prices, and protect profit margins. Cost analysis in MTO — through methods like job costing, variance analysis, and overhead rate analysis — gives manufacturers the visibility they need to understand their true cost structures and make smarter financial decisions. IndustriOS ERP supports this process by centralizing cost data across jobs, materials, and labor, enabling real-time tracking and more precise cost management at every stage of production.

Cost Analysis in MTO Manufacturing: Why It Matters for Profitability

- Job costing helps MTO manufacturers determine order costs and ensure precise pricing.

- Variance analysis identifies cost discrepancies for swift corrective action.

- Overhead and capacity analyses optimize resource use and enhance productivity.

- Profitability and make-or-buy analyses aid in strategic decision-making and growth.

Make-to-Order Recap

MTO manufacturing is characterized by its bespoke approach, where each product is created based on individual customer specifications. This customization demands a flexible production system and a detailed understanding of cost structures to ensure that operations remain efficient and profitable. Unlike mass production, MTO requires precise cost tracking to adjust to varying order demands.

For make-to-order manufacturers seeking to manage their production processes more effectively, Industrios’ ERP solutions offer valuable support in handling cost structures. With software tailored for flexible operations, Industrios helps improve efficiency and profitability. Explore how Industrios can assist your MTO business in achieving practical success.

9 Key Evaluations for Cost Analysis in MTO Manufacturing

Effective cost management in MTO manufacturing hinges on a series of targeted analyses. These analyses help manufacturers dissect their cost structures, identify inefficiencies, and make strategic decisions to enhance financial performance.

#1 – Job Costing in MTO Manufacturing

At the heart of MTO manufacturing is job costing, a critical analysis that itemizes expenses associated with individual orders. This involves tracking materials, direct labor, and overhead costs allocated to each job. By breaking down these components, manufacturers can assess specific orders’ total cost and profitability. Job costing provides the foundation for accurate pricing, ensuring that all incurred expenses are reflected in customer quotes and that profit margins are safeguarded.

#2 – Variance Analysis for Cost Control

Variance analysis helps identify discrepancies between actual and projected costs:

- Compares actual costs against budgeted or standard costs

- Pinpoints reasons for cost variations (e.g., material price changes, labor inefficiencies)

- Enables swift implementation of corrective measures

#3 – Overhead Rate Analysis for Accurate Costing

Due to their indirect nature, managing overhead costs is complex. Overhead rate analysis involves calculating these costs and ensuring they are appropriately allocated to products or orders. This analysis is crucial for achieving accurate product costing and financial transparency. Properly managed overhead rates prevent distortions in cost reporting, support strategic decision-making, and enhance profitability.

#4 – Target Costing in Custom Manufacturing

Target costing shifts the focus to designing products that meet predetermined cost objectives. By setting a target cost derived from subtracting a desired profit margin from a market price, manufacturers are encouraged to innovate and find cost-effective production methods. This analysis promotes efficiency from the outset of product development, ensuring that cost objectives align with market competitiveness. Understanding the cost implications of production volume changes leads us to marginal cost analysis.

#5 – Marginal Cost Analysis for Scaling Decisions

Marginal cost analysis evaluates the costs associated with producing one more unit, which helps manufacturers make informed decisions about scaling production. This insight is pivotal for setting pricing strategies that optimize profitability at different production volumes. Understanding resource allocation becomes essential as production scales, leading to capacity utilization analysis.

#6 – Capacity Utilization Analysis to Optimize Resources

This analysis highlights the costs of underutilization or overutilization, providing a basis for optimizing resource allocation. By fine-tuning capacity use, manufacturers can enhance productivity and reduce costs, leading to more competitive pricing and improved margins.

#7– Profitability Analysis for Sustainable Growth

Profitability analysis examines the financial returns from various products, orders, or customer segments. By identifying which areas generate the most and least profit, manufacturers can strategically allocate resources and focus on high-margin activities. This targeted approach enhances overall business performance and ensures sustainable financial growth.

#8 – Make or Buy Analysis in MTO Manufacturing

A critical decision for MTO manufacturers is to produce components in-house or source them from external suppliers. Make-or-buy analysis compares the costs and benefits of both options, ensuring that production decisions maximize efficiency and cost-effectiveness. This analysis aids in strategic planning and resource optimization. Accurate forecasting is crucial, which is where cost estimation comes into play.

#9 – Cost Estimation for Future Projects

This process involves forecasting future project costs using historical data, current market conditions, and industry trends. Reliable cost estimates enable manufacturers to set realistic prices and manage customer expectations, fostering strong client relationships and ensuring project profitability.

How IndustriOS Handles Cost Analysis in MTO

Running nine different cost analyses is only practical when manufacturers have a system that captures the right data at the right level of detail. IndustriOS ERP is built for make-to-order environments, tracking costs at the individual job level from the moment an order enters the system through final delivery.

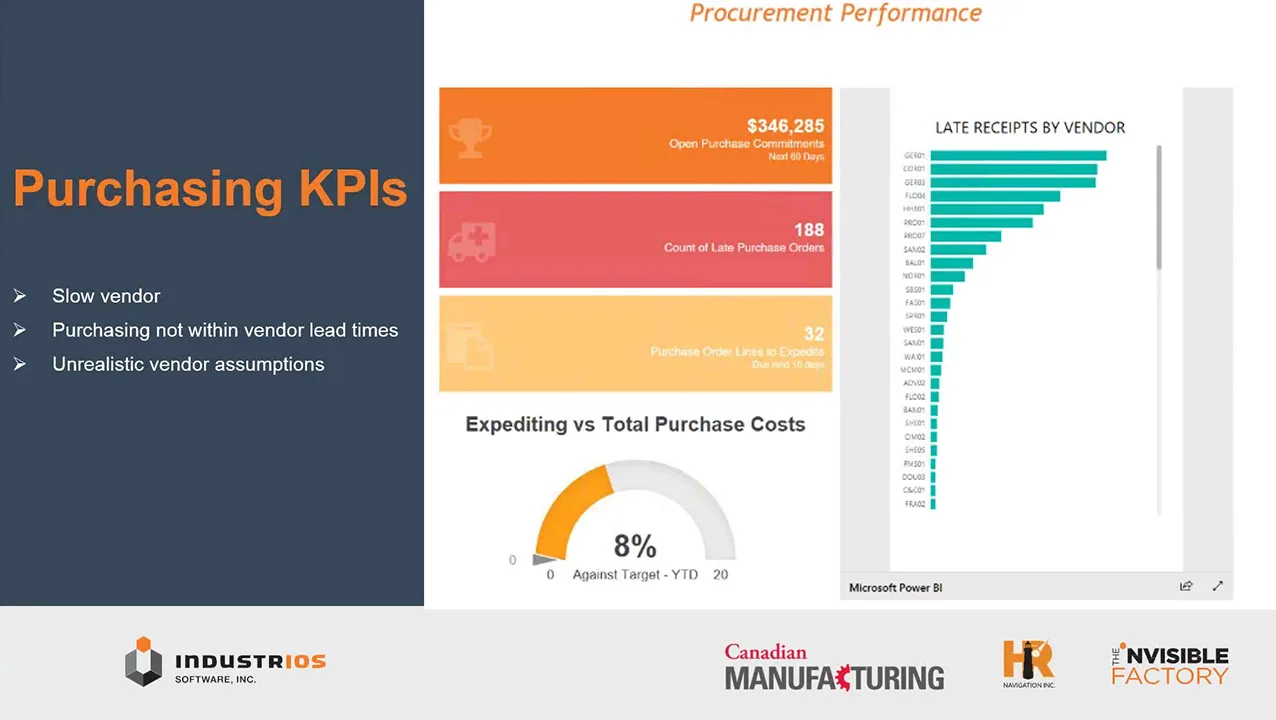

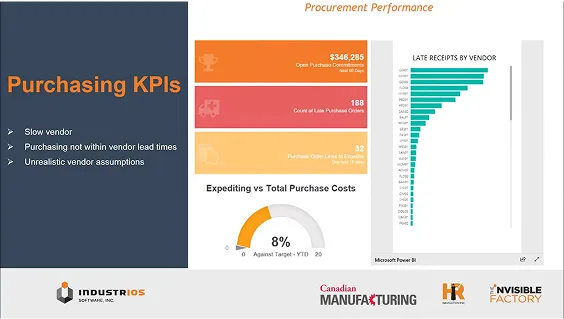

For job costing, IndustriOS ties materials, labor, and overhead directly to each work order, giving manufacturers an accurate picture of what a job costs versus what was quoted. This same job-level data feeds into variance analysis — when actual costs deviate from estimates, the system surfaces discrepancies so teams can correct issues before they compound. Overhead rate analysis also becomes more reliable, since IndustriOS captures machine time, labor hours, and indirect costs in real time rather than relying on outdated averages.

Running nine different cost analyses is only practical when manufacturers have a system that captures the right data at the right level of detail. IndustriOS ERP is built for make-to-order environments, tracking costs at the individual job level from the moment an order enters the system through final delivery.

For job costing, IndustriOS ties materials, labor, and overhead directly to each work order, giving manufacturers an accurate picture of what a job costs versus what was quoted. This same job-level data feeds into variance analysis — when actual costs deviate from estimates, the system surfaces discrepancies so teams can correct issues before they compound. Overhead rate analysis also becomes more reliable, since IndustriOS captures machine time, labor hours, and indirect costs in real time rather than relying on outdated averages.

On the strategic side, reporting and analytics within IndustriOS support profitability analysis by segment, product line, or customer, while the same visibility enables make-or-buy decisions through clear cost comparisons between in-house production and outsourced components.

By centralizing data across procurement, production, and inventory, IndustriOS gives manufacturers the foundation to run cost analysis in MTO as an ongoing part of how they manage and improve operations — not as a one-off exercise.

Final Thoughts on Cost Analysis in MTO

Make-to-order manufacturers benefit significantly from thorough cost analysis to understand cost structures and improve financial performance. By utilizing tools such as job costing, variance analysis, and overhead rate analysis, these manufacturers can gain valuable insights into their operational costs, which supports informed decision-making and boosts profitability.